Let me tell you a little story, the story of Sir Isaac Newton and his stock market adventure. In 1720, Newton, the illustrious scientist, invested in the South Sea Company stocks, attracted by the promise of quick gains. He initially made a profit by selling his shares but later reinvested at a higher price seeing the stock prices continue to rise. The speculative bubble burst, and Newton suffered considerable losses. Later, he is said to have remarked with a touch of bitterness and humor, “I can calculate the movement of heavenly bodies, but not the madness of men.”

This anecdote reminds us of the dangers of speculation in the stock market. Unlike these risky investments, index Exchange-Traded Funds (ETFs) offer a safer and more diversified approach. They allow investors to benefit from market growth without having to predict individual stock movements. In this article, we will explore how index ETFs can be a wise option for saving and investing smartly, avoiding the pitfalls of rampant speculation.

Chasing Illusions

Stock traders are constantly searching for the next gold nugget. Whether it’s artificial intelligence, electric cars, nanotechnology, pharmacology, or the revolutionary new cancer vaccine, it’s often just noise. This perpetual quest pushes you to constantly jump from one position to another, hoping to hit the jackpot. But in reality, predicting the future is a perilous exercise, no matter what metrics you use. Your crystal ball is more likely to blind you than guide you to the rare gem.

Let’s take a moment to revisit the 20th century. Did you know there were about 1,900 car manufacturers? Almost all of them disappeared, swallowed up by fierce competition. By 2000, only General Motors, Chrysler, and Ford had survived, and even these giants had to be bailed out by the government during the 2008 crisis. Imagine trying to analyze every financial report, every cash flow of these thousands of companies… You would be overwhelmed and probably outpaced by the magnitude of the task.

What this story teaches us is that the quest for the rare gem is often a zero-sum game, where the chances of success are slim, and the risks are high. You can’t afford to risk your livelihood on risky bets beyond your control.

Exchange-Traded Funds (ETFs)

Imagine yourself as a team selector for a demanding sports competition. Rather than choosing a single athlete based on their individual performances, you have the option to form a complete and diversified team. Each team member possesses specialized skills that can complement each other: a fast sprinter, a solid defender, a tactical strategist, and so on. Together, they form a robust unit capable of facing different game scenarios.

Exchange-Traded Funds (ETFs) operate on a similar principle. Instead of investing in individual stocks, where a single bad decision can have a significant impact, you invest in an ETF that groups a wide range of stocks and sometimes bonds. Each asset in the ETF contributes to portfolio diversification, thus reducing overall risk. If a specific stock underperforms, others in the ETF can compensate for those losses, stabilizing your long-term investment.

This approach of instant diversification allows investors to maximize their overall success chances by minimizing the impact of individual stock fluctuations on their portfolio.

| Type of ETF | Description |

|---|---|

| Sector ETFs | Include major market sectors representing specific industries, such as financial services, technology, healthcare, etc. |

| Real Estate ETFs | Include several real estate investment trusts (REITs). |

| Fixed Income ETFs | Cover broad markets or sectors of the bond market (corporate, government, or international, for example). |

| Other ETFs | Various types of ETFs covering different assets and investment strategies. |

ETFs are like the diversified team of runners: they maximize your chances of success by investing in a diverse set of assets rather than betting on a single stock. This strategy not only reduces risk but also simplifies portfolio management, allowing you to focus on your long-term financial goals rather than daily market fluctuations.

Here is the table of mentioned ETFs with their main characteristics:

| ETF | Stock/Bond Ratio | Management Fees | Annual Return (1 year) |

|---|---|---|---|

| VTI (Vanguard Total Stock Market ETF) | 100% stocks | 0.03% | 23.20% |

| VFV (Vanguard S&P 500 Index ETF CAD-hedged) | 100% stocks | 0.08% | 28.38% |

| VT (Vanguard Total World Stock ETF) | 100% stocks | 0.07% | 18.55% |

| GRO (Vanguard Growth ETF Portfolio) | 80% stocks / 20% bonds | 0.25% | 10.8% |

| EQT (Vanguard Balanced ETF Portfolio) | 60% stocks / 40% bonds | 0.25% | 10.2% |

| VGRO (Vanguard Growth ETF Portfolio) | 80% stocks / 20% bonds | 0.25% | 10.89% |

| VEQT (Vanguard All-Equity ETF Portfolio) | 100% stocks / 0% bonds | 0.25% | 11.29% |

| VIU (Vanguard FTSE Developed All Cap ex North America) | 100% stocks | 0.23% | 17.60% |

| VXC.TO (Vanguard FTSE Global All Cap ex Canada Index) | 100% stocks | 0.22% | 19.18% |

| HXQ (iShares NASDAQ 100 Index ETF CAD-Hedged) | 100% stocks | 0.28% | 31.09% |

| QQQ.F (Invesco QQQ Trust) | 100% stocks | 0.30% | 36.17% |

This table summarizes some of the discussed ETFs, highlighting their allocation in stocks versus bonds, their management fees (if applicable), and their annual return when available.

Bonds are debt instruments issued by governments or companies to raise funds. They typically pay regular interest and repay the principal at maturity. Considered less risky than stocks, bonds offer increased stability and more predictable returns. They are particularly suitable for conservative investors or those nearing retirement, looking to preserve their capital while generating income.

Bond Allocation Based on Risk Tolerance

| I can tolerate a drop of _ % in pursuit of higher long-term returns | % of my portfolio allocated to bonds |

|---|---|

| 5% | 80% |

| 10% | 60% |

| 15% | 40% |

| 20% | 20% |

| 25% and above | 0% |

Keys to Managing Emotions

-

Simplify Management: Investing in multiple individual stocks can be stressful and difficult to manage. ETFs reduce this complexity by offering instant diversification.

-

Avoid Loss Aversion: Loss aversion is a cognitive tendency where losses have a stronger emotional impact than equivalent gains. For example, imagine that the price of a stock you own suddenly drops. You are emotionally affected and stressed, and you decide under pressure to sell it. A few days later, the price starts rising again, proving it was just a market correction. By diversifying with ETFs, you mitigate this feeling and avoid impulsive decisions.

-

Recognize Cognitive Biases: For example, the confirmation bias pushes us to seek information that confirms our preexisting beliefs. Suppose you invest in a nanotechnology company, convinced you have found the gold nugget. You keep buying shares even in the face of warning signs because you only seek positive information. By systematically investing in ETFs, you reduce the influence of these biases and promote a more rational approach.

Investment decisions are often influenced by emotions, which can compromise rationality. Loss aversion amplifies our reaction to potential losses, sometimes pushing us to make impulsive decisions. Additionally, cognitive biases like confirmation bias push us to seek information that confirms our preexisting beliefs rather than objectively evaluating the facts. ETFs and systematic management offer a more structured and diversified investment approach, allowing you to avoid these emotional and cognitive traps. This reduces the stress associated with managing multiple individual stocks and promotes a focus on long-term financial goals by minimizing the influence of emotions.

Systematic Saving

Systematic saving relies on a regular and disciplined approach to investing. This involves automating periodic contributions to your investment account, whether monthly, quarterly, or annually. This method offers several practical and psychological benefits. Firstly, it helps neutralize the often-harmful emotions in decision-making by preventing impulsive reactions to market fluctuations. Secondly, it establishes financial discipline by helping you maintain a steady pace toward your long-term financial goals while minimizing distractions.

A key aspect of systematic saving is using the Dollar-Cost Averaging (DCA) method. By regularly investing fixed amounts, you buy more shares when prices are low and fewer shares when prices are high. This allows you to cover multiple entry points

, whether the market is up or down. Over the long term, this strategy tends to smooth out market fluctuations and generate overall good performance. By adopting this approach, you give yourself the best chance of success by patiently building your portfolio step by step, with method and determination.

For example, with each paycheck on Thursday, you transfer $291 to your TFSA to then buy an index ETF (VFV). By the end of the year, you will have completed your maximum contribution of $7,000, while having different market entry points thanks to the cost averaging method (DCA).

Fees: The Brake on Your Wealth

When it comes to investing, fees are often the silent enemies of your wealth. Although your bank advisor may tout the merits of complex funds with high fees, it’s important to understand that these fees can seriously limit your portfolio’s growth. Over a 40-year period, annual fees of 2% can reduce your portfolio’s value by nearly 40%. This is a significant erosion of your wealth potential, often masked by financial jargon.

To maximize your wealth, it’s crucial to focus on three wealth creators: the amount invested, time, and the rate of return.

Optimizing Wealth Generators

- Amount: Investing more today and doing so regularly over a long period significantly increases your potential gains.

- Time: Investing is a long-term game. The longer you let your money grow, the more compound interest can work in your favor.

- Rate: Reinvesting dividends increases the overall return of your portfolio (DRIP).

Reducing Wealth Destroyers

- Fees: Reducing investment fees is essential for maximizing returns. Using low-cost ETFs is a good strategy.

- Taxes: Adopting tax-efficient investment strategies helps keep more of your gains (TFSA, RRSP, RESP).

- Inflation: Protecting your portfolio against inflation is crucial for maintaining the real value of your investments.

Here is a simple formula to illustrate the impact of these factors on your future wealth:

Future Wealth = (Amount + Time + Rate) - (Fees + Taxes + Inflation)

When you pay fees, you lose twice: you lose the amount of the fees themselves and you also lose the potential gains that money could have generated if it had remained invested. Annual fees may seem insignificant, but they have a devastating cumulative impact over the long term. Every dollar saved in fees is an extra dollar that can grow thanks to the magic of compound interest. By reducing fees, you increase your total return and fuel the growth of your portfolio over the long term.

Here is a comparison table showing the impact of fees on investments between an ETF (VFV) and a mutual fund from your banker.

For example, you decide to start with an initial investment of $20,000 and add $8,000 annually with an expected return of 8%. Here is the long-term impact of the fees.

| Year | VFV Balance (with 0.08% management fee) | Banker’s Mutual Fund Balance (with 1.66% management fee) | Difference |

|---|---|---|---|

| 1 | $29,584.00 | $29,268.00 | -$316.00 |

| 2 | $40,560.65 | $39,630.79 | -$929.86 |

| 3 | $52,406.66 | $50,650.58 | -$1,756.07 |

| 4 | $65,190.86 | $62,369.03 | -$2,821.83 |

| 5 | $78,987.58 | $74,830.43 | -$4,157.15 |

| 6 | $93,877.00 | $88,081.88 | -$5,795.12 |

| 7 | $109,945.65 | $102,173.47 | -$7,772.19 |

| 8 | $127,286.95 | $117,158.46 | -$10,128.49 |

| 9 | $146,001.68 | $133,093.51 | -$12,908.17 |

| 10 | $166,198.61 | $150,038.84 | -$16,159.77 |

| 11 | $187,995.14 | $168,058.50 | -$19,936.64 |

| 12 | $211,517.95 | $187,220.61 | -$24,297.34 |

| 13 | $236,903.78 | $207,597.60 | -$29,306.18 |

| 14 | $264,300.16 | $229,266.49 | -$35,033.67 |

| 15 | $293,866.33 | $252,309.18 | -$41,557.15 |

| 16 | $325,774.14 | $276,812.78 | -$48,961.36 |

| 17 | $360,209.05 | $302,869.91 | -$57,339.14 |

| 18 | $397,371.21 | $330,579.07 | -$66,792.14 |

| 19 | $437,476.61 | $360,044.98 | -$77,431.63 |

| 20 | $480,758.36 | $391,379.03 | -$89,379.33 |

| 21 | $527,468.02 | $424,699.66 | -$102,768.36 |

| 22 | $577,877.09 | $460,132.82 | -$117,744.27 |

| 23 | $632,278.55 | $497,812.44 | -$134,466.11 |

| 24 | $690,988.61 | $537,880.95 | -$153,107.66 |

| 25 | $754,348.51 | $580,489.80 | -$173,858.71 |

| 26 | $822,726.51 | $625,800.05 | -$196,926.46 |

| 27 | $896,520.05 | $673,982.98 | -$222,537.08 |

| 28 | $976,158.04 | $725,220.70 | -$250,937.34 |

| 29 | $1,062,103.36 | $779,706.89 | -$282,396.47 |

| 30 | $1,154,855.54 | $837,647.51 | -$317,208.04 |

This table clearly shows the significant impact fees can have on the growth of your investment over the long term.

Beware of your banker’s cross-selling practices. This means they tend to recommend specific financial products, like mutual funds, not only to meet your needs but also to maximize their commissions. Your advisor will never recommend alternatives like index ETFs, which often have much lower fees and can be more beneficial for you in the long run. It’s like a personal trainer advising you to eat junk food instead of recommending a balanced and healthy diet. Understand that even small percentages of annual fees, like 2%, can significantly reduce your portfolio’s growth over several decades. Every dollar saved in fees represents an extra dollar that can increase your long-term potential gains.

Beating the Pros Effortlessly: The Art of Lazy Investing

To illustrate the inefficiency of actively managed funds, let’s examine the data from the SPIVA report. This report reveals that 91% of Canadian equity fund managers have underperformed their benchmark index (S&P) over the past decade. This means that the vast majority of these managers, despite their complex strategies and hours of research, failed to outperform a simple benchmark index.

Rather than worrying about selecting the right actively managed fund, a simple and effective solution is to invest in an ETF that replicates this benchmark index, such as VFV. By doing so, you can outperform the majority of actively managed funds without spending hours analyzing strategies or researching individual stocks. You can then focus on other aspects of your life, knowing that your investment is on track to follow market growth.

Index ETFs

Let’s take the analogy of a cyclist to understand index ETFs. Imagine you are a passionate spectator of the Tour de France, observing the cyclists’ performances throughout the stage. Opting for an individual cyclist involves conducting extensive research: evaluating their race history, current physical condition, race strategies, and other relevant criteria. It’s an intense time investment to identify the best among the many competitors.

In contrast, betting on the peloton, the lead group composed of the best cyclists in the race, represents a solid alternative strategy. This group stands out clearly from the rest of the peloton, always ahead thanks to their talent and strategy. They represent the elite of the competition, capable of overcoming the most challenging obstacles with their experience and cooperation.

Similarly, investing in an index ETF means buying a share of a diversified portfolio of stocks that track a specific market index, like the S&P 500

or a sector index. Choose an index ETF to benefit from the collective performance of a basket of diversified stocks, similar to the collective strength and resilience of the lead peloton in a cycling race. This approach reduces risk by mitigating the impact of individual stock fluctuations, offering an effective strategy for investors seeking to stabilize and grow their portfolio over the long term.

Conclusion

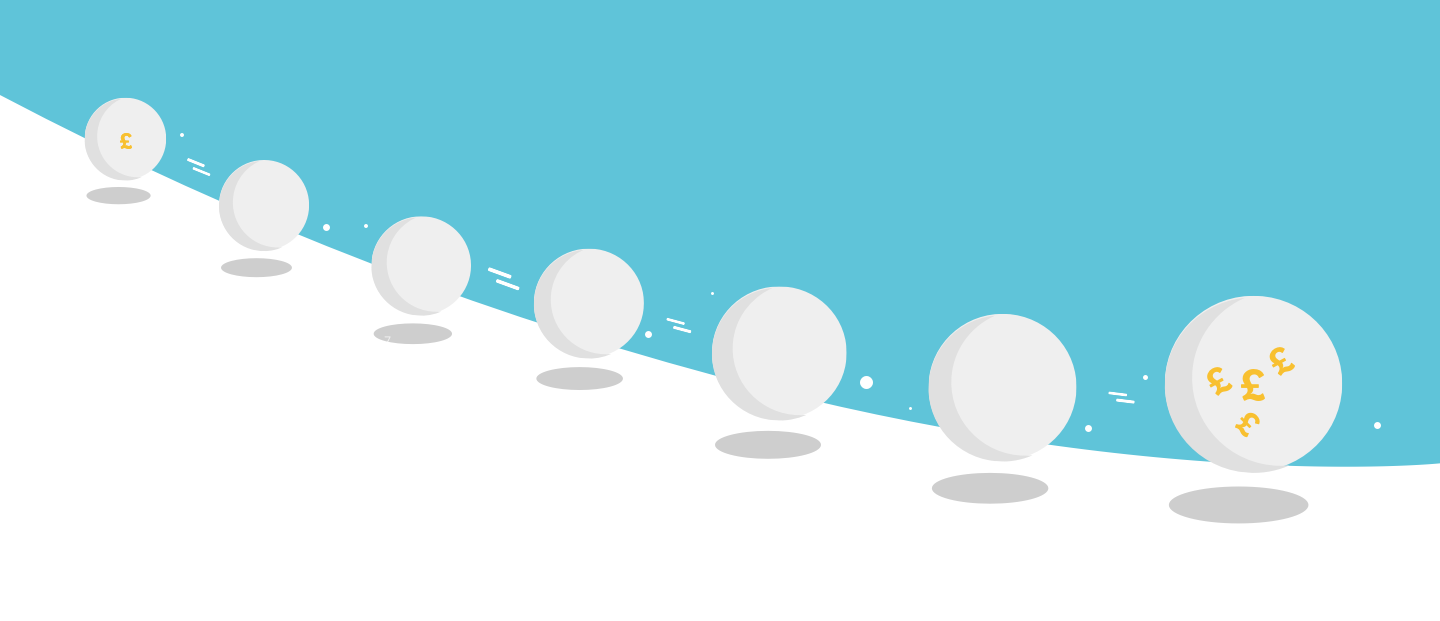

At the end of this exploration, you will have understood: investing is a long journey that spans many years. Just like a snowball that grows as it rolls down a hill, your portfolio can grow exponentially through dividend reinvestment. However, human emotion can often be a major obstacle on this path. To remedy this, automating saving and systematic investing, favoring low-cost index ETFs, allows you to maximize income while preserving your gains from the eroding effects of high fees. This approach not only reduces the stress associated with financial management but also strategically positions you to achieve your long-term financial goals more safely and effectively.

To ensure you maintain a disciplined and emotionally healthy approach to your finances, you will now only open your checking account once a year to calculate your annual balance. The rest of the time, you can serenely dedicate yourself to your pleasurable activities, knowing that your automatic saving and investment strategy is in place to work in your favor.